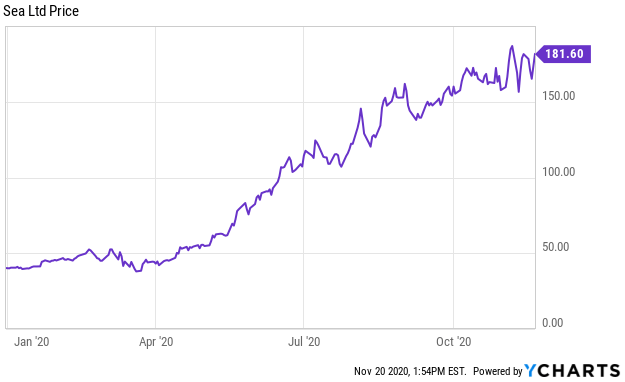

In the business world, a commonly heard phrase is “The growth is in China.” No doubt when we look east, the massive Chinese market (with its more than 1.4 billion people and rapidly increasing disposable income) is a shining beacon of opportunity. The likes of Alibaba (BABA) and Tencent Holdings (OTCPK:TCEHY) are testament to that growth, but perhaps have also dominated the headlines (thereby overshadowing others in the making). Sea Limited (SE) is an example of a hidden gem, tucked in a less conspicuous corner of the globe. This stock is up over 300% this year, but has substantially less coverage. In this article, we look at the business, key drivers of growth and conclude with our opinion on investing.

Populous region, growing demand for games and digital services

Sea operates primarily in Southeast Asia, the region south of China, east of India, and north-west of Australia. Nestled around the South China Sea, the region includes countries like Indonesia, Vietnam, Thailand, Philippines, Cambodia and Singapore. Collectively, Southeast Asia has about 670 million people, and a GDP of $3.4 trillion, and one of the world’s fastest growing regions in terms of GDP per capita. Internet penetration rates have grown meaningfully over time, and there are about 483.2 million internet users today, the majority of which access the internet on their smartphones. By 2025, the region is projected to have 594.3 million users accessing the internet for video games, streaming media, e-commerce and fintech services. By comparison, the United States has about 284 million internet users, a little more than half of Southeast Asia.

Online games have seen phenomenal traction in the region. Many internet cafes have pivoted to focus on video-gaming and hosting local competitions. Revenue from the industry has surged in recent years, and gamers are spending more time playing games or watching them. It is no surprise that Esports is extremely popular in the region, and one of the most important growth drivers for the games industry in Asia. According to Niko Partners, an “overwhelming majority” of gamers are active in esports games. PC and mobile game revenue for the greater Southeast Asia region (which includes Chinese Taipei), is projected to grow at a CAGR of 13.5% from $5 billion in 2019 to $8.3 billion by 2023.

E-commerce and digital payments are likewise significant opportunities. As internet penetration grows, millennials and the younger generation in the region have been highly receptive to using the internet for online shopping, streaming media and financial services. Older users are also adapting well to using technology for their businesses and personal transactions. Even in countries like Indonesia where internet penetration rates are lower, a survey from market research firm Datareportal.com highlighted that 96% of respondents aged 16 to 64 have searched online for a product or service to buy, while 79% have made an online purchase via a mobile phone. This is encouraging to know as Indonesia is the region’s largest market. Digital payments and fintech services, a complementary business to e-commerce, have also experienced healthy adoption momentum. A high percentage of an unbanked population and an increasing desire to transact online have fueled demand for these services. A recent Google-Temasek-Bain report mentioned that the digital financial services industry in the region is projected to grow at a 22% CAGR between 2019 and 2025 to reach $38 billion in revenue by the end of the period.

Market leadership in a competitive and diverse area

Sea Limited’s business is centered on these major high-growth areas. The company has three key operating segments:

-

Garena Digital Entertainment, an online games and social platform;

-

Shopee, an e-commerce marketplace; and

-

SeaMoney, its digital financial services business.

Garena earns its revenue mostly from sales of in-game items. Although it has developed its own game (Free Fire), most of Garena’s business is positioned in a high revenue, low risk part of the gaming value chain. It obtains licenses to the most popular gaming titles, localizes content, hosts and manage game operations, as opposed to the riskiness of game creation or low margins of game distribution. Garena has had tremendous success in Southeast Asia, becoming the number one platform by market share in the region with 570 million active players as it holds the licenses to the world’s leading game titles, making it an essential venue for avid gamers to discover and play popular games.

Similarly, Shopee is also leading the region as one of the most popular shopping apps. Gross Merchandise Value (GMV), or the total value of goods sold on its e-commerce marketplace, has expanded more than 15x in a mere three years, reaching $17.6 billion at the end of 2019. During that same period, the number of orders processed on its platform has increased more than 16x to 1.2 billion orders. The company faces competition from regional players like Lazada (backed by Alibaba), global e-commerce brands like Amazon, and local players like Indonesia’s Tokopedia and Bukalapak. Yet despite the tough competitive landscape, Shopee is winning the region, ranking first in the shopping category by the number of downloads, average monthly active users, and total time spent in app according to data from App Annie, a leading global provider of mobile data and analytics. Shopee was also the second most downloaded app globally.

It is worthwhile to mention here that Southeast Asia is a very diverse region. While countries are located close to one another, they each have very different languages, ethnic composition, foods, culture, and economic levels. Consumer preferences vary significantly, as with business practices and regulatory policies. Operating a business in this region is challenging, but Sea Limited has managed to achieve a consistently, strong competitive position across its major markets. This is impressive performance for a fairly young company.

Moving to a lead position (Source: Datareportal)

Attractive content draws users and deepens engagement, drives monetization opportunities

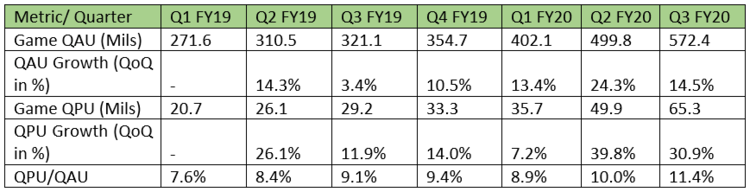

Sea Limited’s tremendous success can perhaps be best attributed to its ability to draw and deepen engagement of its users on its platforms. Garena, through strategic partnerships with prominent game developers and investors (Tencent Holdings is one of them), holds exclusive licenses to run leading game titles for the region. Many of these titles are immersive games that are highly engaging, and statistically, result in gamers playing more frequently, and for longer periods of time, in addition to spending more money on in-game purchases. We can see this from the growing number of game quarterly active users (QAU) and game quarterly paying users (QPU). Crucially, the number of QPUs is rising faster than QAUs, increasing the QPU as a percentage of QAU. Revenue per QPU is also trending up quarter-on-quarter, which explains the explosive sales growth of 167% for its digital entertainment segment in FY 2019. The company has also done exceedingly well in proprietary game development, launching a battle royale genre mobile game titled Free Fire in 2017, which has received very positive reception in Southeast Asia and Latin America, and driving a solid revenue stream for the company. Free Fire is the highest grossing mobile game in these two regions, sustained by a steady roll-out of attractive content to keep users interested and e-sports tournaments. The success of Free Fire is a promising indication of Sea’s ability to complement its licensed games with proprietary game generation capabilities, free of revenue sharing agreements and potentially less favorable partnership agreements.

source: Factset, Earnings Presentation

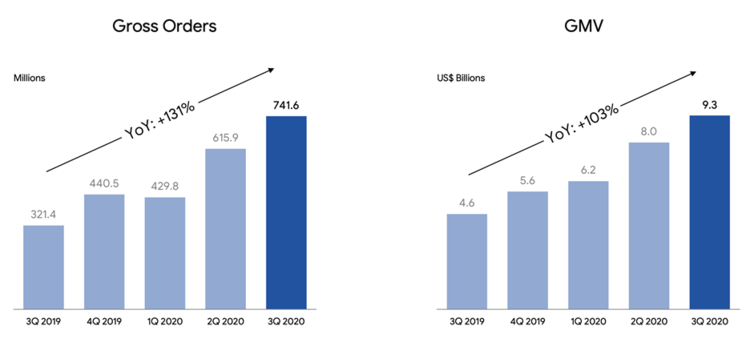

On the e-commerce front, Shopee is a platform of choice for many sellers and buyers within the region, many of them long-tail, small business owners. It offers several value-added and seller support services that are important for these smaller businesses, including business management tools, advertising placement, integrated payment, logistics, fulfillment and customer service capabilities, making it a one-stop solution. New features are constantly added and enhanced. For example, as live-streaming catches on, a streaming tool for sellers to live-stream and sell their merchandise was added to the app. Making the platform easy and relevant for its sellers to run their business on Shopee has reaped rewards for the company as its seller base expands rapidly, in turn attracting more buyers. Apart from the broad range of products available for sale at competitive prices, buyers are also drawn to the Shopee app for its gamifications features (e.g. Shopee Games, Shopee Coins) and unique events (e.g. streaming of a popular K-pop music festival recently), which has enhanced user engagement and social activity. Platform traction has driven robust GMV and order growth over time, while average order values (AOVs) remain steady in the low to mid-teens range. Monetization opportunities are growing as Shopee broadens its range of seller services, and progressively introduces higher transaction commissions and fee-based programs.

Shopee Performance (Source: Company Presentation)

As for SeaMoney, the segment has also gained momentum, increasing total payment volume (TPV) and the number of quarterly paying users. Leveraging the broad user base of both Garena and Shopee, this is a highly synergistic part of the business that can grow organically and rapidly with little need for heavy user acquisition expenses, and a target consumer base that is mostly greenfield ie. potential users are not currently using an alternative digital payment system. Both Garena and Shopee users have been using the SeaMoney digital wallet to pay for their transactions.

Impressive topline improves profitability but makes valuation pricey

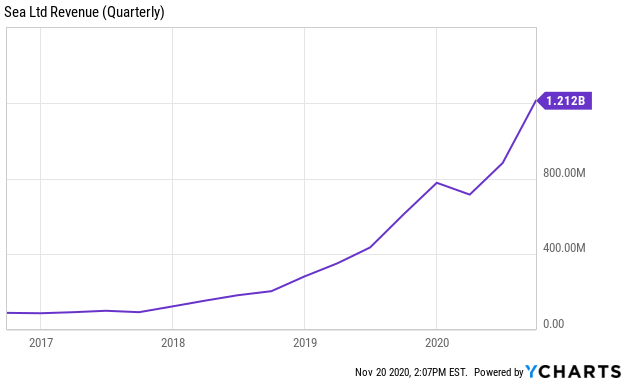

The result of deeper engagement is greater monetization rates for Sea Limited. This has led to the robust revenue growth the company consistently reports. Between FY16 and FY19, revenue rose at a CAGR of 84.5%, accelerating to triple-digit growth in FY19. Strong topline performance has lifted margins for Sea Limited, and it just started turning adjusted EBITDA positive on a consolidated group basis in Q2 and Q3, and achieved its first full year of positive operating cash flow last year. This is good news for investors who often have to contend with deeply negative profitability and cash flows in exchange for high sales growth rates. Sea Limited’s profitability comes from its Garena digital entertainment segment, which has offset the cash burn from its younger Shopee and SeaMoney businesses. Garena is expected to continue delivering strong sales performance in the near to medium term, supporting the growth investments required for e-commerce and digital financial services until they scale sufficiently to become profitable.

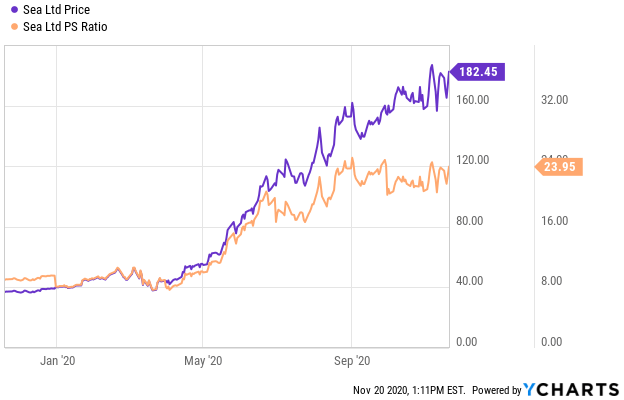

The company’s impressive performance over the last few quarters have also driven up its valuation to its all-time historical highs. At a trailing P/S ratio of 23.95x, the stock is trading expensively, but not without good reason. Sea Limited is projected to deliver another triple-digit sales growth this fiscal year, and its competitive position never looked better. Operating metrics suggest increasing traction and engagement across its platforms, and the business is just starting to penetrate the Latin American market. Profitability is improving even as it invests heavily on growth.

A long-term play: We are just getting started

Looking ahead, we think Sea Limited has a lot more ground to cover. Its gaming business is just beginning to gain momentum in new geographies like Latin America, another region with more than 600 million people. E-commerce penetration is still relatively low in Southeast Asia, with significant opportunities for more brick-and-mortar retail services to shift online and the company to monetize its services. As for SeaMoney, the region is just getting acquainted with digital payments and financial services, many still transacting in cash.

Some question the sustainability of its growth as the tailwinds for its business from the pandemic start to weaken. Sea Limited’s business benefitted from Covid-19 as demand for online shopping and digital payments grew. Lockdowns also meant people were spending more time at home on online games. Q3 was a litmus test for the company as the region was mostly out of quarantines during the quarter. Even as restrictions lifted and Covid-19 cases in low numbers, the company did not find engagement declining materially across its platforms. Revenue grew 98.7% YoY in Q3 as gamers continue spending more on Garena, and GMV on Shopee and use of its digital wallet continue to tick upwards. Management even raised sales guidance for the full year FY20. This signals an enduring demand for its services that was already poised to occur but accelerated by the pandemic. We believe that Sea Limited can maintain its explosive pace of growth in the near to medium term.

More thoughts on Sea Limited

To add more color on Sea, Left Brain’s, Janice Quek recently discussed the company on our weekly podcast (link here). Janice lives in Singapore, and gives you the inside scoop on this rapidly growing Southeast Asia Internet company–including online shopping, digital payments and mobile games.

Left Brain Thinking Podcast, Janice on Sea Limited.

Conclusion

Sea Limited is a rapidly growing internet business in the right place at the right time. Its leadership positions in digital entertainment (Garena) and online marketplace (Shopee) will allow it to continue to rapidly grow into a very large total addressable market. Further, SeaMoney helps it expand its leadership position. For these reasons, we’ve included Sea as a top idea on our recent digital transformation top idea list. The company is still in its early stages of growth, with plenty of room and opportunities to expand. We see Sea Limited as a long-term growth story that will likely continue to impress investors with its performance.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: Left Brain Investment Research has no positions in any of the aforementioned securities. However, affiliate companies Left Brain Capital Management and/or Left Brain Wealth Management are long Sea Limited (SE).

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.