kokkai/iStock Unreleased via Getty Images

Investment thesis

Sea Limited (SE) is currently one of my highest conviction ideas due to the company having multiple high growth drivers in both the near and long term:

1. Garena, as a market leader, will serve as a cash cow with solid growth.

2. Leadership position in Southeast Asia e-commerce is currently in the early days and likely to see strong growth in the future from increasing penetration in the region brought about by multiple tailwinds.

3. The company’s recent entry into the Latin America (LatAm) e-commerce market brings exposure to an under penetrated, fast growing market. It has also more recently entered new geographies in Europe and India.

3. New emerging fintech business, Sea Money, will bring additional high growth areas with strong digital payments tailwinds.

With Sea Limited being down 46% from its all time high, I believe that expectations for Sea has been reset and have turned too bearish. I have a high conviction in the company, giving Sea a rating of Strong Buy. Based on my DCF model, my target price for Sea is $422.71, implying a solid 115% upside potential.

Overview

Sea Limited has 3 main operating segments.

First, Garena is Sea’s gaming segment. Garena is one of the global leaders in online games development and publishing. Its most iconic self-developed game was Freefire, which was the most downloaded mobile game in the world in 2019 and 2020.

Second, Shopee is Sea’s e-commerce segment. Shopee is the largest e-commerce player in Southeast Asia and Taiwan. In Southeast Asia, Shopee gets 343 million visits per month, while the second largest player, Tokopedia, gets less than half the site visits.

Lastly, Sea money is Sea’s financial services and payment segment. It is currently also the leading financial services and payment provider in South East Asia.

Shift in mix to emerging, high growth e-commerce and fintech business

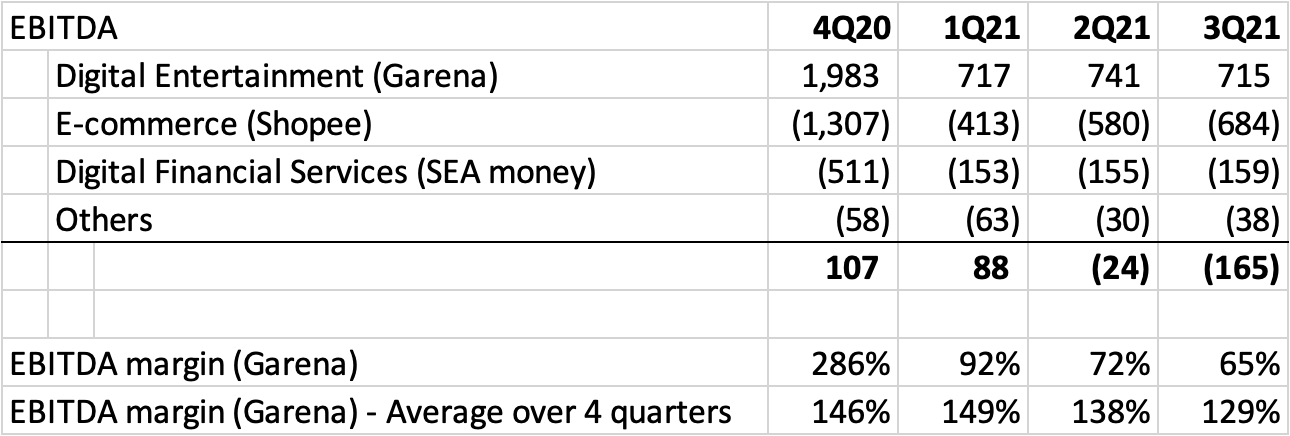

Before 2020, Sea was valued more for its gaming segment, Garena, which contributed 52% of Sea’s revenues and generated $1 billion in EBITDA in 2019. However, as shown in the table below, Shopee and Sea Money have seen strong growth during the pandemic in 2020 and 2021. As of 3Q21, they contribute 54% and 5% of Sea’s revenues respectively.

Source: Author created table using annual reports.

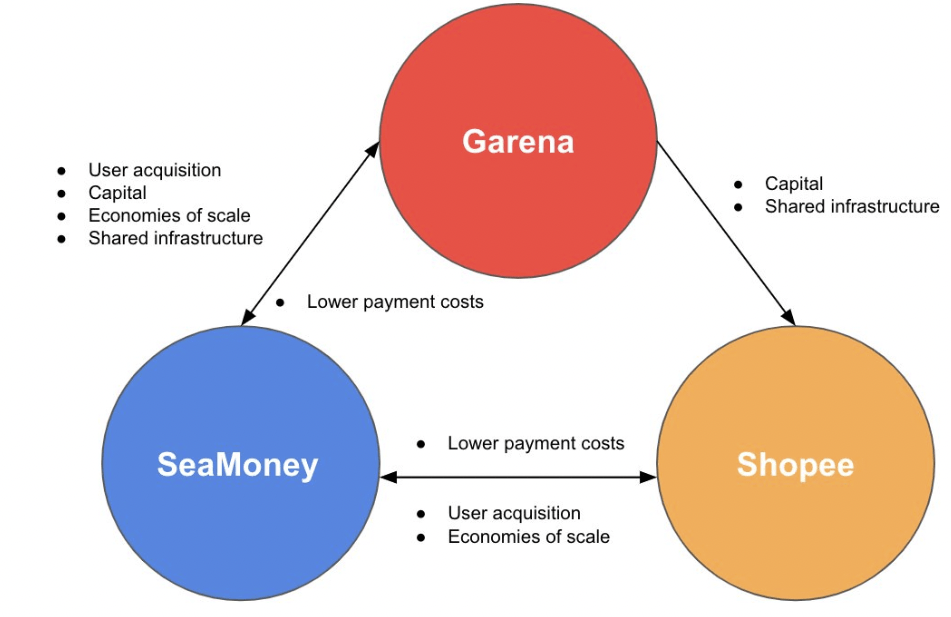

With the acceleration of its e-commerce business, Shopee, Sea’s largest segment contributing to revenues in 2021 was e-commerce and investors are beginning to assign a large portion of SE’s intrinsic value to its e-commerce segment. With its solid ecosystem of e-commerce, digital payments & financial services, and gaming businesses, Sea is able to benefit from the flywheel effect and each business is able to generate huge momentum for future growth of Sea. Source: Manan Joshi

Source: Manan Joshi

Garena as Sea’s cash cow

Garena was founded in 2009 and has been operating for more than 12 years. The largest contributor to Garena’s revenues comes from its self developed game, FreeFire. Garena is EBITDA positive and has seen strong EBITDA margins of 65% in 3Q21.

Source: Author generated from company reports.

Source: Author generated from company reports.

Furthermore, it is worth noting that Garena is still seeing solid operational metrics in 2021, with bookings growth of 27% year on year in 3Q21 and paying user growth surpassing active user growth in the last 4 quarters.

Source: Author generated from company reports.

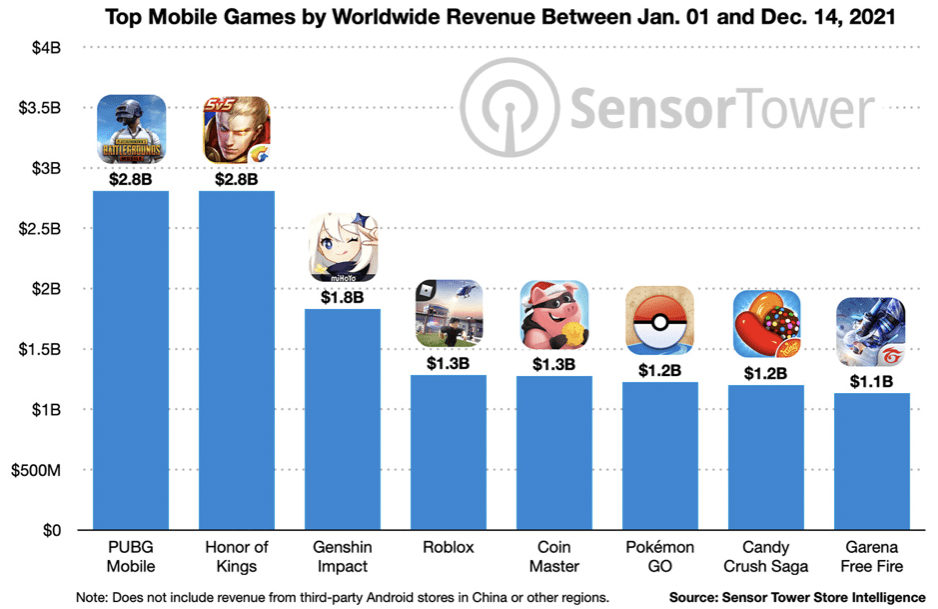

Comparing Garena’s Free Fire to other top mobile games in the world, it is worth noting that Free Fire was the top 8 mobile games by worldwide revenues in 2021.

Source: Sensor Tower

Source: Sensor Tower

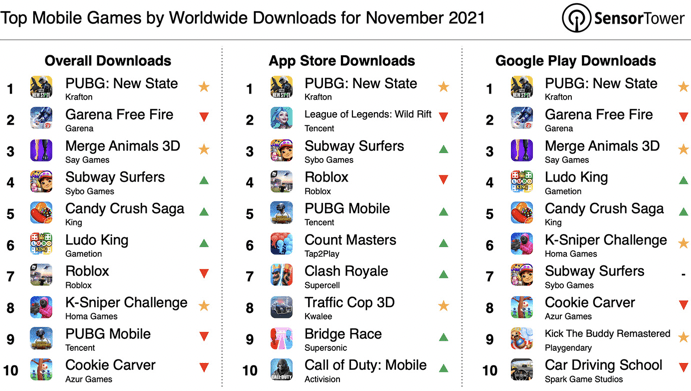

When looking at the top mobile games by downloads, Garena’s Free Fire was the second most downloaded in November 2021.

Source: Sensor Tower

I believe that what these strong download and revenue numbers show for Garena’s Free Fire demonstrate continued strong interest in the game, after its huge successes in 2019 and 2020. Also, Free Fire was found to have one of the highest levels of engagement of the top mobile battle royale games, as well as a massive following of more than 150 million monthly active users.

Based on these, I am of the opinion that after its huge success earlier in 2019 and 2020, the game is sticky in nature with its high engagement levels and active users, and thus, I believe that there is a long runway for Garena’s Free Fire. All in all, due to its high profitability, I expect Garena to continue to grow by 20% CAGR over the next few years, while maintaining its superior EBITDA margins.

Shopee Southeast Asia – Leader in core markets

Shopee is the market leader in Southeast Asia e-commerce market. To illustrate its dominance in the region, Shopee took up 57% of the entire Southeast Asian e-commerce transaction value.

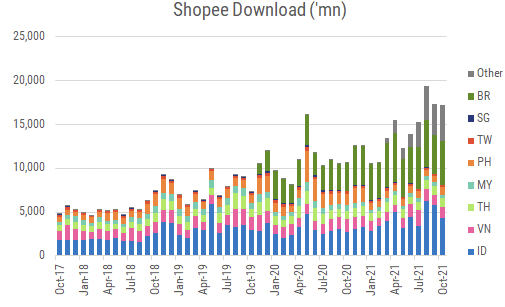

To illustrate what a mammoth task this is, you have to understand that Southeast Asia is a very fragmented region with varying preferences and demographics, ranging from a small, relatively wealthy population in Singapore, to one of the largest population and relatively less developed Indonesia. As such, I believe that Shopee’s ability to succeed in the region is testament to its ability for international expansion. As shown below, Shopee downloads have almost quadrupled in 2021, with success across geographies in South East Asia

Source: Sensor Tower and Goldman Sachs Investment Research

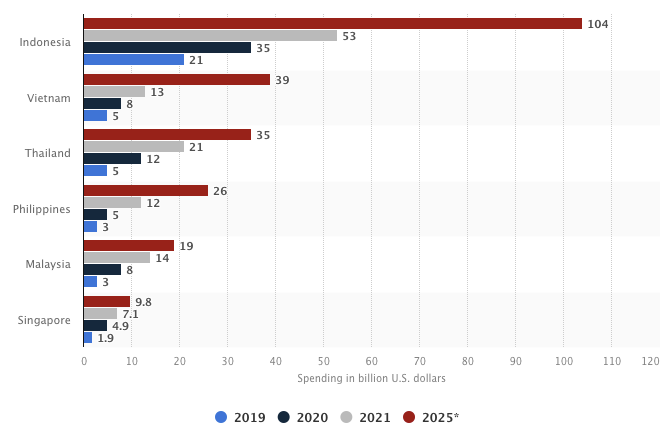

By 2025, the Southeast Asian e-commerce market is expected to be $230 billion, with the trend accelerated by the pandemic. This implies a 18% CAGR over the period, with most of the growth coming from Indonesia, Vietnam, as shown below. The increase in e-commerce penetration in Southeast Asia is due to the increasing use of internet in the region as it becomes part of consumers daily lives. For example, the region now has 440 million internet users, with 350 million of them being digital consumers that have bought at least one online service. In fact, since the pandemic, Southeast Asia added 60 million new digital consumers and this number is expected to creep upwards. As the market leader in the region, I believe that Shopee will continue to see superior growth rates above the industry average and thus could see growth of more than 100% during the same period, implying CAGR of 20% over the period.

Source: Statista

Source: Statista

Shopee new markets: LatAm, Europe and India to demonstrate Shopee’s international expansion abilities

Amazon was arguably the only one e-commerce platform able to be successful in international expansion, while Alibaba’s Lazada’s international expansion plans seems to have faltered and lost to Sea.

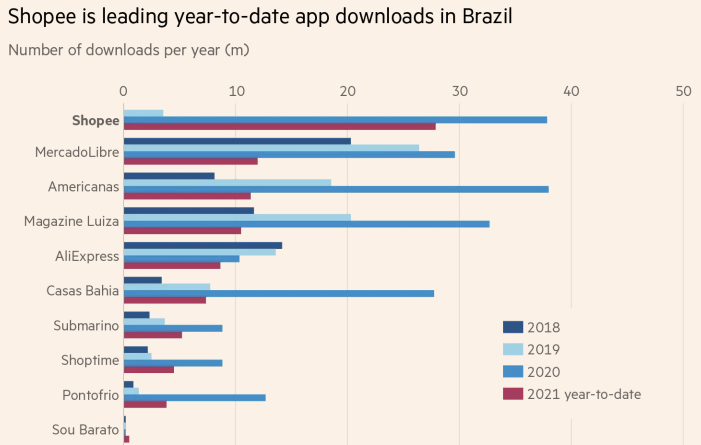

Shopee announced plans for LatAm expansion earlier in the year. although it has been in Brazil since 2019, it had a rather modest start. That said, it became the most downloaded e-commerce app in Brazil in just 2 years, with downloads in 2021 far exceeding any other competitor, including MercadoLibre, the current leader in Brazil. In fact, the app downloads for Shopee are more than double any other player for 2021 year to date.

Source: Financial Times, Sensor Tower and Goldman Sachs Investment Research.

Source: Financial Times, Sensor Tower and Goldman Sachs Investment Research.

Shopee has multiple levers to pull in LatAm. Currently in Brazil, the average price of items sold on its platform is only 40 reais, which is less than a third of MercadoLibre which sells higher value branded items. Shopee is able to increase its average revenue per user (ARPU) by increasing the basket size of shoppers in LatAm, thereby increasing transaction size in LatAm and growing in market share. Of course, it can also focus on growing Mostly Active Users (MAUs) in the earlier stages since it is rather new in the region.

I believe that Shopee’s experience in Southeast Asia provides a playbook for international expansion. Be it increasing mindshare among consumers, adapting its playbook to local conditions, focusing on growth, I believe that it could be able to replicate its success in winning over Alibaba in Southeast Asia in LatAm.

However, I think 1 of the key challenge for Shopee in LatAm is the logistical challenge. MercadoLibre has built a logistics network that covers 90% of Brazil, for example, while Shopee as a new entrant, does not have delivery capabilities and relies on the Brazil postal service which could result in disruptions or slower deliveries.

In India, Shopee is dipping its toes in the e-commerce market there, ramping up on hiring and recruiting vendors to sell on Shopee India’s platform. Similarly for Shopee started its Europe expansion in Poland in September 2021, subsequently entering Spain and France in October 2021. There are early positive signs for Shopee in Europe as Shopee was top shopping app in Poland and Spain as of October 2021, according to App Annie., beating local e-commerce platform Allegro in Poland and global platforms like Amazon in Spain.

In my opinion, the expansion into international markets in LatAm, India and Europe is a great opportunity for a leading e-commerce player in Southeast Asia to expand its footprint in other regions. In my view, it does not need to be the largest player in all of these new markets. In fact, I am forecasting a modest 5% market share in these new regions by 2025, just to be conservative. However, as long as Shopee shows signs of becoming a market leader in one of these regions, Sea’s share price could rerate to one of an international leader in e-commerce.

Digital payments and financial services an emerging business in Sea

Sea money aims to provide convenient transactions, digital payments and flexible financing solutions. For this fintech business, Sea’s current focus is to expand the use cases so that the service can serve more businesses and value add to consumers. Sea has partnered with more online and offline merchants in recent months like GooglePay in Malaydoa and Blue Bird in Indonesia. Sea is also looking outside of its wallet business by looking at new initiatives like buy now pay later, digital bank and insurance tech, all of which are in the early development stages.

Tencent’s reduction in stake in Sea

Tencent announced that it would reduce its voting power in Sea to less than 10% by converting all of its Class B ordinary shares into Class A ordinary shares. Additionally, it plans to reduce its stake in Sea from 21.3% to 18.7%. With this, Li, Sea’s founder, chairman and CEO will see his voting power increased from the current 52% to 57%.

First, I believe that it was a matter of time before Sea reduced Tencent’s control over Sea due to Sea’s goal to expand globally. It was reported earlier that Sea had planned to reduce the control Tencent had over the company as it sets its aim of expanding globally.

Second, Li already had substantial and the majority of voting power before this and with the Tencent’s reduction in voting power in Sea, Li would be in an ideal position for the next phase of expansion for Sea.

Third, Tencent’s recent JD.com sale shows that Tencent itself is making changes to its own portfolio of investments to ensure that they are more focused and is not seen as anti competitive.

Financials

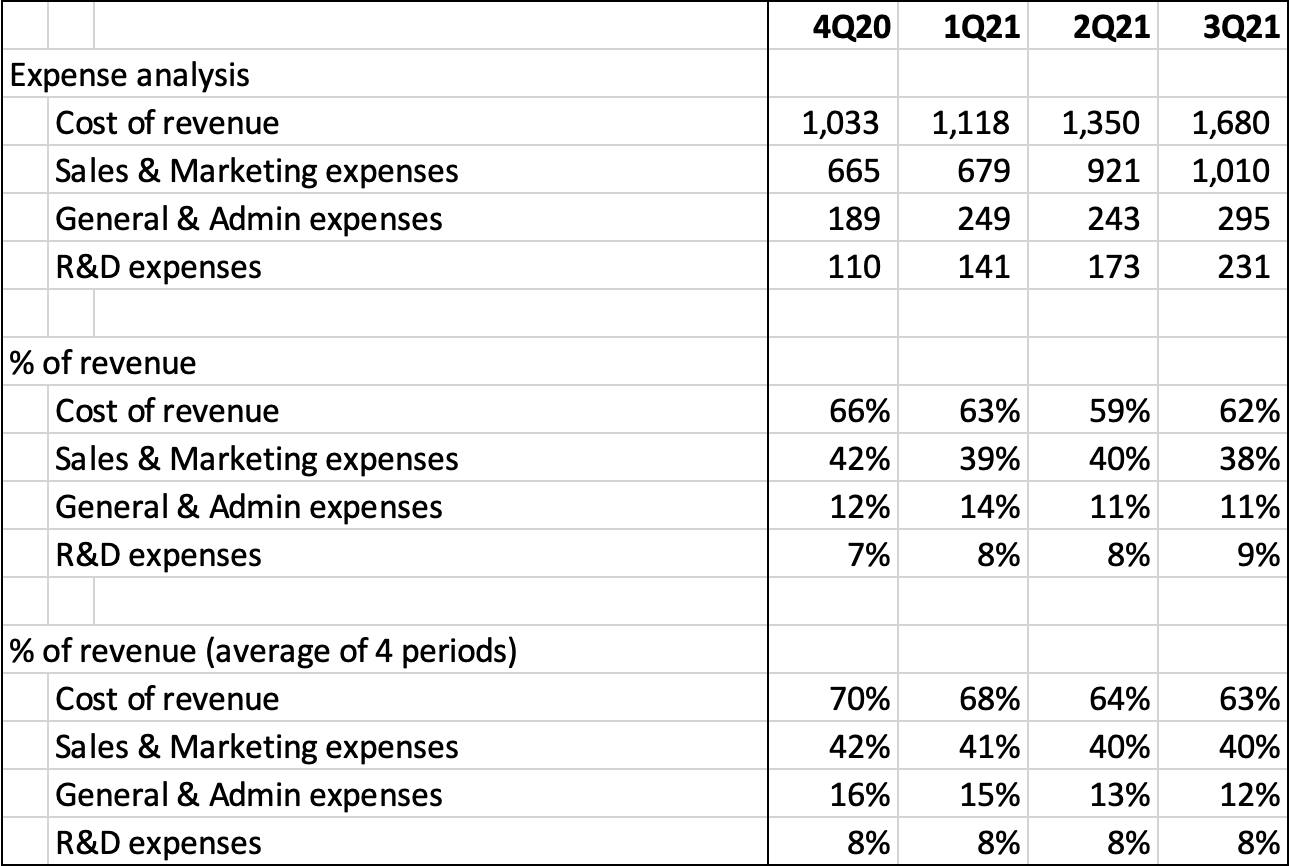

Sea is currently -6% EBITDA margin in 3Q21, mainly due to negative EBITDA margins of Shopee and Sea Money. When looking deeper into the expenses of Sea, there are some positives:

1. Cost of revenues have been declining from 70% in 4Q20 to 63% in 3Q21, implying that as the business scales, gross margin improvements are probable.

2. Additionally, sales & marketing and general & admin expenses have seen their proportions fall as a percentage of revenue as well, showing better signs of cost control in the Group.

3. Lastly, Sea has maintained 8% R&D expenses over the last 4 quarters, which I believe is crucial for Sea as a technology enabled platform.

Source: Author generated from quarterly reports.

Valuation

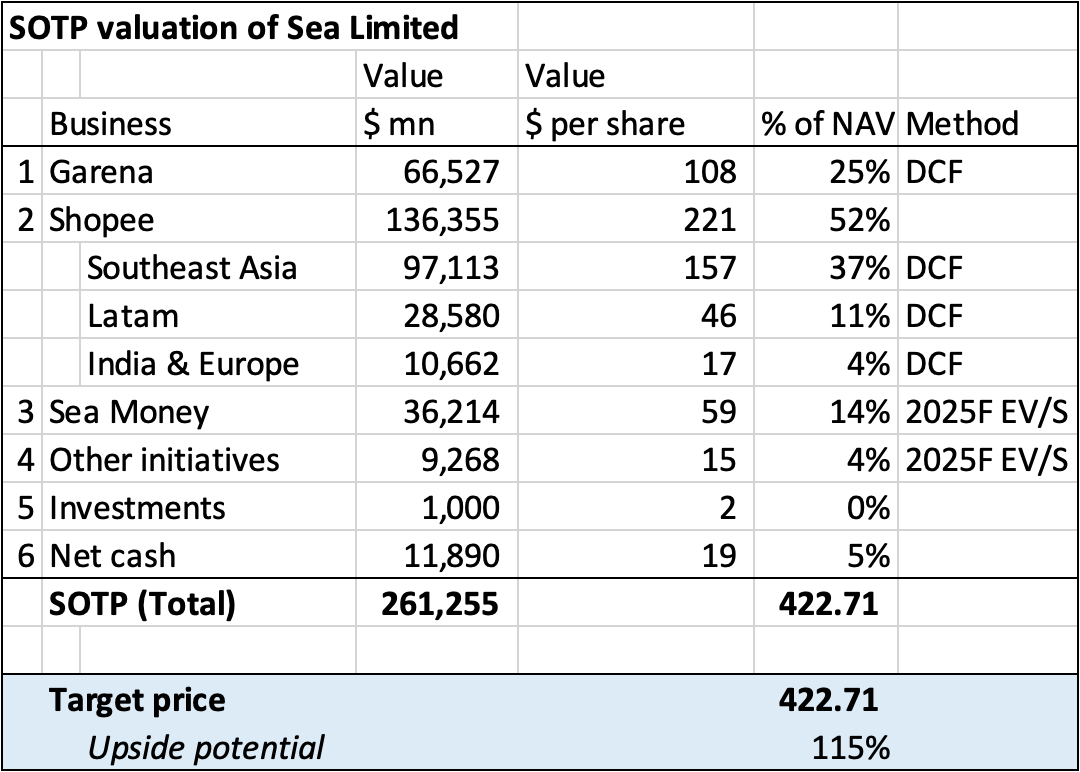

I have done up a SOTP valuation for Sea Limited, based on DCF of each segment over the next 10 years. Shopee remains the largest part of Sea’s NAV at more than 50% while Garena makes up a quarter of Sea’s NAV. My assumptions for India, Europe and LatAm are conservative, in my view, with only 5% market share assumption by 2025. Sea could prove to be much stronger in these new markets but I am being conservative due to the uncertainty in execution in new markets.

Based on my SOTP valuation, the derived target price is $422.71, implying a 115% upside potential from today’s prices.

Relative valuation

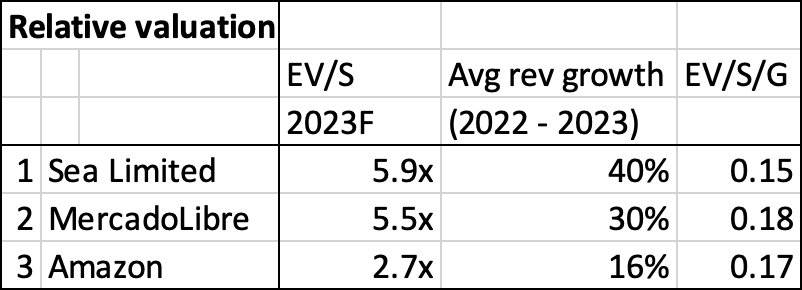

Apart from looking at the SOTP valuation, I think that relative valuation can provide us with some insights into Sea’s valuation compared to competitors in the industry. Based on its 2023 EV/Sales of 5.9x and higher revenue growth profile, Sea Limited has lower EV/S/G (EV/Sales proportionate to revenue growth) than MercadoLibre (MELI) and Amazon (AMZN), implying Sea is trading at about 16% discount to peers despite its strong business fundamentals and flywheel competitive advantage.

Sea Limited is trading at 5.9x FY2023 EV/S, growing at 40% revenue growth. Its main competitor and leader in LatAm, MercadoLibre, is currently trading at 5.5x FY2023 EV/Sales, rev growth at 30%while Amazon trading at 2.7x FY2023 EV/S, with revenue growth at around 18%

Risks

Competition

Sea’s business segments, especially Shopee, could see fierce competition from global peers as the industry gets crowded. For example, Shopee has done well in Southeast Asia but the threat of Tokopedia in Indonesia is still there. Furthermore, Alibaba’s Lazada is ramping up and focusing on international expansion as China’s domestic e-commerce market slows. If competition intensifies, this could be a significant drag to profitability of the e-commerce segment.

Execution in new markets

The operating and competitive environment in LatAm, India and Europe has its challenges. Although Shopee has had a good run in Southeast Asia, there are still execution risks in these new markets especially with large domestic e-commerce players already present.

Synergies in all 3 business segments

The flywheel effect could prove to be Sea’s competitive advantage if it is able to build its gaming, e-commerce and fintech ecosystem well. However, if synergies between the 3 are not reaped, the company is not maximising the benefit of its entire ecosystem and should each segment operate increasingly in silos, this could result in deterioration of competitive advantage of Sea.

Conclusion

In my view, I see Sea as the leader in not just Southeast Asia, but also likely to be a leader in international expansion in the e-commerce space. Its wildly popular Free Fire game, as well as gaming business Garena looks set for continued success with the high engagement of its large number of MAUs, and with that, looks set to continue providing necessary funds for Shopee’s expansion into new markets as well as fortify its position in the Southeast Asia e-commerce market. Lastly, the many new initiatives outside of Sea Money’s wallet business looks set to further strengthen the flywheel effect and create a competitive advantage that no other global peer can match. With a target price of $422.71, this implies a 115% upside potential and Sea Limited is one of my high conviction ideas and thus, rated a strong buy.